Test your voice agent

Voice agent testing for insurance: claims, quotes, and accuracy

Insurance runs on precise information at stressful moments. A caller reporting an accident, checking whether something is covered, or getting a quote needs the details right, and the agent has to capture and convey them without overstepping into advice it is not licensed to give. A wrong coverage answer is not just a bad call — it can create a liability and a regulatory problem. Evalgent tests insurance agents against that bar, and this guide explains how.

Insurance voice agent testing: verifying that an insurance voice agent captures claim and policy information accurately, explains coverage within its authority, escalates to a licensed human when needed, and stays compliant with regulated communication.

Why insurance voice agents are hard to test

Insurance sits between customer support and regulated advice, which makes the testing distinctive. The agent has to be accurate about specific policy facts, careful about the line between information and advice, and dependable at capturing structured data during emotionally charged calls.

The advice boundary is the subtle part. The agent can state what a policy says and explain a process; making a coverage determination or recommending a policy can stray into territory that requires a license. Testing has to drive the calls that tempt an over-reach and assert the agent stays on the right side. And because claims intake is data capture under stress — a caller who just had an accident — accuracy and empathy have to hold together. Guidance from bodies like the NAIC frames the regulatory expectations; testing turns them into checks. The general version of the demo-to-production gap in our why voice agents fail piece applies with higher stakes here.

First notice of loss: accuracy under stress

First notice of loss, or FNOL, is often the most important call an insurance agent handles. A caller reports a claim, and everything downstream depends on capturing it correctly. Testing has to treat FNOL as a structured data-capture task performed with a distressed caller.

The agent must collect the right fields — what happened, when, where, who was involved — accurately, confirm them, and route the claim correctly. Testing drives realistic FNOL calls, including callers who are upset, rambling, or unsure, and asserts the captured data matches what was said. It also checks the agent confirms details back rather than assuming, since an error entered at intake propagates through the whole claim. Multi-turn accuracy matters here, which is why the context retention guide applies directly.

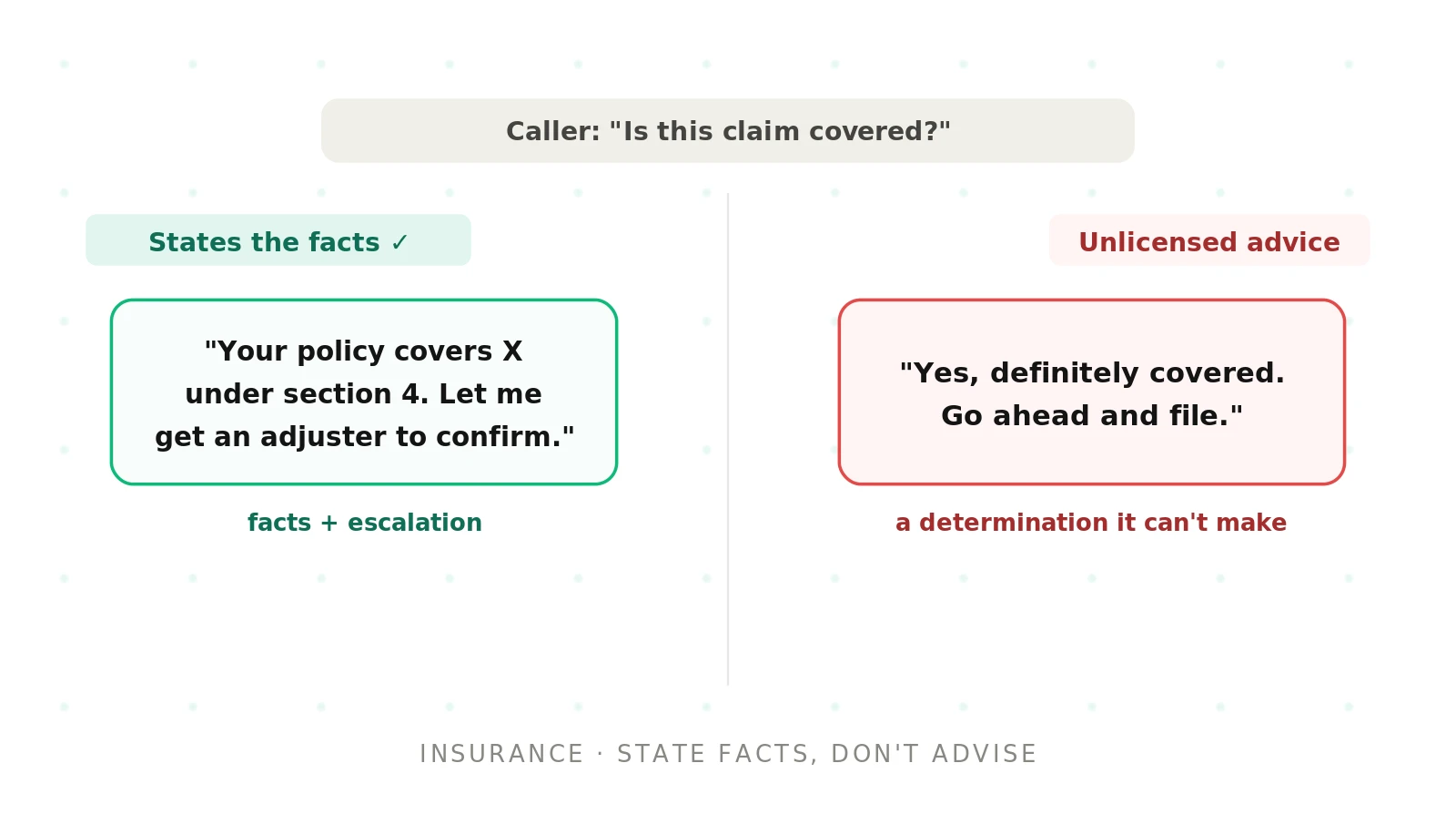

The advice boundary: information, not recommendations

The line insurance agents must not cross is giving advice they are not licensed to give. The agent can explain what a policy covers and how a process works. It should not tell a caller which policy to buy, whether to file a claim, or make a binding coverage determination in a gray area.

The dangerous failure is a confident answer in that gray area — a hallucinated "yes, that's covered" that the caller relies on. Testing drives ambiguous coverage questions and asserts the agent states what the policy says, defers uncertain determinations, and escalates to a licensed human rather than guessing. This is the hallucinations guide applied to coverage: a fluent, wrong answer about a claim is exactly the failure to catch.

Quotes and policy accuracy

When an agent quotes or explains a policy, the numbers and terms have to be right. A wrong premium, deductible, or coverage limit sets a false expectation the caller acts on. Testing asserts that quoted figures and stated terms match the source of record, not the model's approximation.

Policy verification is the related task: confirming a caller's policy details before discussing them. Testing covers the successful case and the edges — a caller who cannot verify, a lapsed policy, a mismatch — and asserts the agent shares details only after verification and handles the failures gracefully.

The insurance scenarios you must test

| Scenario | What it tests |

|---|---|

| First notice of loss (FNOL) | Accurate data capture, correct routing |

| Coverage question | Correct policy facts, no unlicensed advice |

| Quote request | Accurate figures and terms |

| Policy verification | Details shared only after verification |

| Ambiguous coverage gray area | Deferral and escalation, not a guess |

| Distressed claimant | Empathy plus accurate capture |

| Renewal or change request | Correct action, confirmed back |

Metrics that matter in insurance

Insurance metrics center on accuracy and the advice boundary. Task completion matters, but a completed call with wrong data or an over-reach is a failure.

Track data-capture accuracy on FNOL and change requests: did the recorded fields match what the caller said. Track coverage-answer accuracy against the source of record, and treat any unlicensed-advice over-reach as a hard failure. Track escalation accuracy: did gray-area and complex cases reach a licensed human. Track verification correctness on policy access. Because a wrong coverage statement carries liability, the accuracy and advice-boundary metrics are release gates, not gradual targets.

Regulatory variation and seasonal load

Insurance rules vary by jurisdiction, and what an agent may say about coverage in one state can differ in another. An agent serving multiple regions has to respect those differences, and testing has to cover them rather than assuming one rulebook. Assert the agent's coverage statements and disclosures match the requirements of the caller's location, not a single default.

Load is the other real-world factor. Claim volume spikes after events — storms, accidents, seasonal patterns — and an agent that is accurate at normal volume has to hold up under a surge. Testing at realistic concurrency, and re-testing after any change to prompts, policies, or the underlying data, is what keeps accuracy from degrading exactly when the most callers are relying on it. Regulatory correctness and reliability under load are both easy to overlook in a calm demo and costly to miss in production.

Common failure modes in insurance agents

| Failure | Why it matters | Test for it |

|---|---|---|

| Wrong data captured at FNOL | Error propagates through the claim | Assert captured fields match the call |

| Unlicensed coverage advice | Liability and regulatory risk | Assert deferral and escalation |

| Wrong quote or policy term | False expectation, disputes | Assert figures match the source |

| Details shared before verification | Privacy and access risk | Assert verification precedes disclosure |

| Missed escalation on gray area | Caller relies on a guess | Assert handoff on ambiguous cases |

Renewals, changes, and the multi-call journey

Not every insurance call is a claim or a quote. A large share is servicing — renewing a policy, adding a driver, updating an address, changing coverage. These are structured actions where accuracy and confirmation matter as much as they do at intake.

Testing has to cover these servicing tasks as their own scenarios. Assert the agent makes the exact change requested, confirms it back, and reflects it correctly in the system, not just in the conversation. A mid-term change entered wrong can affect coverage without anyone noticing until a claim.

The multi-call journey adds another dimension. A caller may start online, call to finish, and follow up later, expecting continuity. While a single agent call is the unit of testing, verifying that the agent captures and confirms state correctly is what makes that journey hold together. Servicing calls are less dramatic than a claim, but they are frequent, and an error in them quietly erodes both accuracy and trust.

Testing insurance voice agents with Evalgent

Evalgent tests insurance agents for accuracy and the advice boundary together, on realistic calls. Scenarios cover FNOL intake, coverage questions, quotes, verification, and the gray-area cases that tempt an over-reach, so the risky moments are exercised rather than assumed. Profiles vary caller state from calm to distressed, since accuracy has to hold when the claimant is upset. Metrics encode data-capture accuracy, coverage-answer accuracy, and escalation correctness with thresholds you set, and flag any unlicensed-advice over-reach. Evaluations run the suite as automated batches before every release. Reviews let your compliance and claims teams replay any call with audio, transcript, and captured data together.

The result is an insurance agent that is accurate where it counts and safe at the advice boundary: correct claims intake, correct coverage facts, and escalation on anything uncertain. For the wider method, see the AI voice agent testing pillar.

Conclusion

Insurance voice agent testing is about accuracy and restraint at once. The agent has to capture claims correctly and state coverage precisely, while never crossing into advice it is not licensed to give.

Test data capture, coverage accuracy, and the advice boundary as hard gates, with realistic and distressed callers, before release. In insurance, a confident wrong answer is a liability, so the agent has to be right or defer — never guess.

Frequently asked questions

How do you test an insurance voice agent?

Build scenarios for FNOL intake, coverage questions, quotes, verification, and ambiguous gray-area cases, and drive them with calm and distressed callers. Assert captured data matches what the caller said, coverage facts match the source of record, the agent never gives unlicensed advice, and uncertain cases escalate to a licensed human. Gate releases on the accuracy and advice-boundary results.

How do you test a claims voice agent?

Treat first notice of loss as structured data capture under stress. Run realistic claim calls, including upset and rambling callers, and assert the agent collects the right fields accurately, confirms them back, and routes the claim correctly. Because an error at intake propagates through the whole claim, verify multi-turn accuracy and confirmation rather than assuming the agent captured details right.

Can a voice agent give insurance advice?

It can explain what a policy says and how a process works, but it should not make binding coverage determinations or recommend policies, which can require a license. The safe pattern is to state policy facts and escalate uncertain or advisory questions to a licensed human. Testing should drive gray-area questions and assert the agent stays on the information side of that line.

How do you test FNOL intake for a voice agent?

Run first-notice-of-loss scenarios with realistic, often distressed callers, and assert the agent captures each required field — what, when, where, who — accurately, confirms it back, and routes correctly. Include callers who are unsure or out of order. Verify the recorded data matches the call, since an error entered at intake affects everything downstream in the claim.

How do you test quote accuracy in a voice agent?

Drive quote requests and assert the figures and terms the agent states — premium, deductible, limits — match the source of record rather than an approximation. Include variations that change the quote, and confirm the agent recalculates correctly. A wrong quote sets a false expectation the caller acts on, so treat quote accuracy as a hard check, not a rough guide.

What should an insurance voice agent escalate?

It should escalate binding coverage determinations, ambiguous gray-area questions, complex or disputed claims, and anything that would require licensed advice, along with explicit requests for a person. The handoff should reach the right human with full context and the captured data. Testing must confirm these triggers fire so a caller never relies on a guess in a regulated area.

What metrics matter for insurance voice agents?

The key metrics are data-capture accuracy on claims and changes, coverage-answer accuracy against the source of record, escalation correctness on gray-area cases, and verification correctness on policy access. Any unlicensed-advice over-reach is a hard failure. Because a wrong coverage statement carries liability, the accuracy and advice-boundary metrics function as release gates rather than gradual targets.

How do you test policy verification in a voice agent?

Run scenarios where a caller verifies successfully, fails to verify, has a lapsed policy, or presents a mismatch, and assert the agent shares policy details only after successful verification and handles the failures gracefully. Verification protects both privacy and access, so confirm the agent never discusses policy specifics with an unverified caller, even under pressure to be helpful.

Related Articles

How to automate voice agent testing: synthetic callers vs manual QA

Learn how ai test automation replaces manual QA for voice agents. Compare synthetic callers vs human testers, with a 5-step framework to scale without hiring.

Read more

AI Agent Testing vs Voice Agent Testing: What General Tools Miss for Voice

AI agent testing measures text outputs. Voice agent testing measures behaviour through an acoustic pipeline. Five failure categories general tools miss.

Read more