Test your voice agent

Voice agent testing for collections: FDCPA, disclosures, and tone

In collections, a voice agent operates inside one of the most heavily regulated conversations in business. Every call carries required disclosures, prohibited actions, and rules about who the agent may talk to and when. A friendly, capable agent that skips a disclosure or discusses a debt with the wrong person is not a minor bug — it is legal exposure. Evalgent tests collections agents against these rules directly, and this guide explains how.

Collections voice agent testing: verifying that a debt collection voice agent executes required disclosures, contacts only the right party, respects frequency and conduct rules, and handles disputes and hostility while staying compliant.

Why collections voice agents are harder to test

A collections agent is judged less on how helpful it sounds and more on whether it followed the rules. That inverts the usual testing priority. The conversation is procedural and legally bound, so the questions are specific: did it give the mini-Miranda disclosure, did it verify it was speaking to the right party, did it stop when asked.

The callers make it harder. People in collections are often stressed, defensive, or hostile, and they will push the agent off-script, dispute the debt, or demand it stop calling. The agent has to hold both its composure and its compliance under that pressure. A demo with a cooperative caller proves none of this. The Regulation F rules that govern debt collection assume the hard calls, so testing has to reproduce them.

FDCPA and Regulation F: what testing has to prove

The core of collections testing is compliance. The Fair Debt Collection Practices Act and its implementing Regulation F set out what a collector must say, must not say, and must not do. A voice agent has to follow all of it, and testing turns each rule into an assertion.

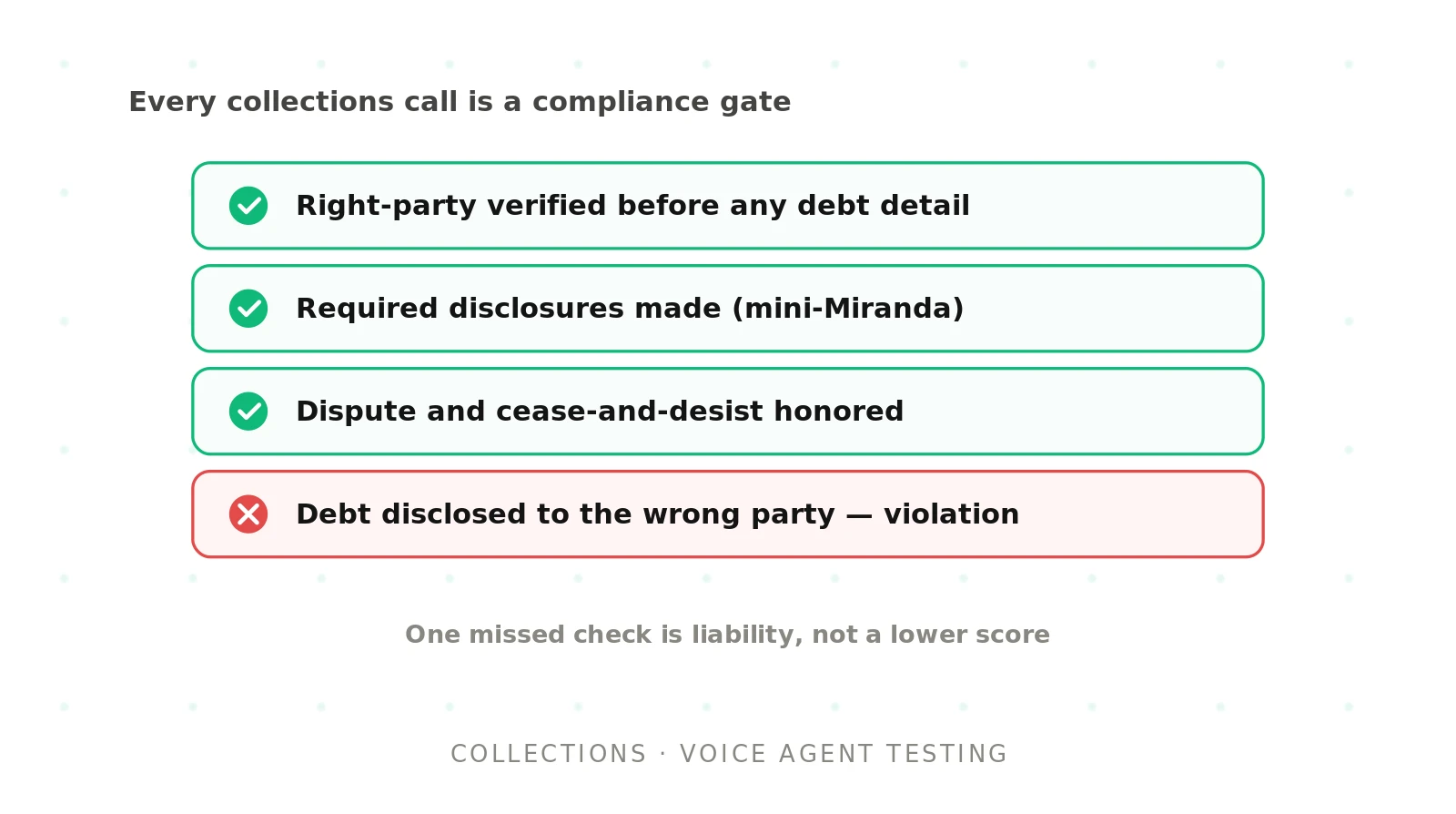

The required disclosures are the starting point. The agent typically must identify that it is attempting to collect a debt and that any information will be used for that purpose — the mini-Miranda — and provide validation information. Testing asserts these fire, in the right place, on the right calls. Prohibited conduct is the other side: no threats, no harassment, no false statements, no discussing the debt with unauthorized third parties. Testing drives the situations that tempt those failures and asserts they never happen.

Regulation F also added specific limits, including on call frequency and on how and when a consumer can be contacted. A voice agent that dials or continues within a call needs to respect those boundaries, and testing should confirm it does. Because these are legal requirements, they belong in a release gate as binary checks, exactly the discipline described in our SOP-based voice agent testing guide.

Right-party contact and third-party disclosure

One of the highest-risk moments in a collections call is confirming who is on the line. The agent may only discuss the debt with the consumer, and disclosing it to anyone else can be a violation. This is right-party contact, and it deserves its own tests.

The agent has to verify identity before revealing any debt details, and it has to handle the ambiguous cases: a family member answering, a wrong number, a workplace line, someone who claims to be the consumer but is not. Testing drives each of these and asserts the agent withholds debt information until the right party is confirmed, and handles a wrong party without disclosure. This mirrors the identity and disclosure discipline in our prompt injection guide, where the risk is being talked into revealing something the agent should protect.

Disputes, cease-and-desist, and stopping

Consumers have rights that override the collection flow, and the agent must honor them instantly. If a caller disputes the debt, the agent has to follow the dispute process rather than pressing for payment. If a caller invokes a cease-and-desist or asks the agent to stop contacting them, the agent must comply and route accordingly.

These are exactly the moments an under-tested agent gets wrong, because they interrupt the happy path. Testing has to insert a dispute or a stop request mid-call and assert the agent changes course correctly — not that it keeps pushing its script. Handling these right often means escalating to a human or a specific workflow, which is why the escalation guide applies directly to collections.

The collections scenarios you must test

A strong collections scenario set covers the compliance moments and the difficult callers together.

| Scenario | What it tests |

|---|---|

| Right-party verification | Debt disclosed only after identity confirmed |

| Wrong party or third party answers | No debt disclosure to unauthorized people |

| Required disclosures | Mini-Miranda and validation fire correctly |

| Debt dispute raised | Agent follows dispute process, stops collecting |

| Cease-and-desist request | Agent complies and stops contact |

| Hostile or abusive caller | Agent stays professional and compliant |

| Payment plan negotiation | Accurate terms, no false promises |

Metrics that matter in collections

Collections metrics are dominated by compliance, and most are binary. A disclosure either fired or it did not. The right party was verified or was not.

Track disclosure compliance as a pass-or-fail rate across calls. Track right-party contact accuracy: correct verification, and correct withholding when the party is wrong. Track dispute and cease-and-desist handling: did the agent honor the request immediately. Alongside these, track conduct under pressure — whether the agent stayed professional with a hostile caller — and the business metric of successful, compliant resolutions. The compliance metrics are release blockers; a single systematic disclosure miss is not a quality dip, it is liability.

Ambiguous rights and partial requests

Not every consumer states their rights cleanly. Some say they might dispute, ask the agent to stop calling for now, or question the debt without formally disputing it. These ambiguous signals are where compliant agents and risky ones diverge.

The agent has to recognize a rights-adjacent request even when it is indirect, and handle it correctly — neither ignoring it nor over-reacting and halting a valid collection. Testing has to include these partial and conditional phrasings, not just the textbook "I dispute this debt" or "cease and desist." Assert the agent surfaces the right path — a dispute process, a documented stop request, or an escalation — for each. Real consumers rarely use the exact words a script expects, so an agent that only handles explicit invocations of rights will mishandle the messy, ambiguous majority, which is exactly where regulatory complaints originate.

Common failure modes in collections agents

| Failure | Why it is dangerous | Test for it |

|---|---|---|

| Missed or misplaced disclosure | FDCPA violation | Assert disclosures fire on the right calls |

| Debt disclosed to wrong party | Third-party disclosure violation | Assert verification before any detail |

| Ignoring a dispute | Regulatory and legal exposure | Assert the dispute process triggers |

| Ignoring cease-and-desist | Prohibited continued contact | Assert contact stops on request |

| Losing composure with hostility | Harassment risk, brand damage | Test hostile-caller profiles |

Call timing, frequency, and records

Regulation F did more than shape what a collector says; it constrained when and how often contact can happen. A voice agent that places or continues calls has to respect reasonable-hour limits and the frequency presumptions the rule introduced, or it creates the same exposure as a prohibited disclosure.

Testing has to treat timing and frequency as compliance checks. Assert the agent does not attempt contact outside permitted hours for the consumer's location, and that repeated-contact logic stays within the rule's boundaries. Where the agent schedules follow-ups or callbacks, confirm those respect the same limits.

Records are the other half. Collections is audited, so every call needs a complete, accurate trail: what was disclosed, who was verified, what the consumer requested. Testing should confirm the agent produces that record and that sensitive details within it are handled correctly. An agent that behaves compliantly but cannot prove it leaves the collector exposed when a call is later questioned.

Testing collections voice agents with Evalgent

Evalgent tests collections agents where the compliance risk actually lives — on hard, adversarial calls. Scenarios script right-party verification, required disclosures, disputes, cease-and-desist requests, and hostile callers, so the compliance moments are exercised, not assumed. Profiles vary caller tone from cooperative to abusive, since composure under pressure is part of compliance. Metrics encode disclosure compliance, right-party accuracy, and dispute handling as pass-or-fail gates with thresholds you set. Evaluations run the full suite as automated batches before every release. Reviews let your compliance team replay any call with audio, transcript, and metrics together, which is where a collections agent gets signed off.

The result is an agent your compliance and legal teams can approve: disclosures made, the right party protected, disputes honored, and professionalism held under fire. For the wider method, see the AI voice agent testing pillar and the SOP-based voice agents piece.

Conclusion

Collections voice agent testing is compliance testing first and conversation testing second. The agent has to make the right disclosures, protect the right party, honor disputes and stop requests, and stay professional with callers who are anything but.

Treat every compliance behavior as a hard, pass-or-fail gate, tested against realistic and hostile callers before release. In collections, an untested agent is not a quality risk — it is legal exposure waiting for the wrong call.

Frequently asked questions

How do you test a collections voice agent?

Build scenarios for the compliance moments — right-party verification, required disclosures, disputes, and cease-and-desist requests — and for difficult callers. Drive them with profiles that range from cooperative to hostile, and assert each rule holds: disclosures fire, debt is withheld from the wrong party, and stop requests are honored. Gate every release on the compliance results.

Is a debt collection voice agent FDCPA compliant?

Not automatically. Compliance depends on whether the agent makes required disclosures, contacts only the right party, respects conduct and frequency rules, and honors disputes and cease-and-desist requests. Testing proves these behaviors hold on real, adversarial calls, turning FDCPA and Regulation F requirements into concrete assertions you can gate releases on rather than assume.

How do you test disclosure compliance in a voice agent?

Drive calls that require the mini-Miranda and validation disclosures, and assert they fire in the right place on the right calls, every time. Include variations where a caller interrupts or redirects, and confirm the disclosure still occurs. Track disclosure compliance as a pass-or-fail rate, and treat any systematic miss as a release blocker rather than a minor issue.

How do you test right-party contact?

Run scenarios where the consumer, a family member, a wrong number, and someone falsely claiming to be the consumer each answer. Assert the agent verifies identity before revealing any debt detail, and withholds information from anyone unverified. Right-party contact is one of the highest-risk moments in collections, so it deserves dedicated, adversarial tests rather than a single happy-path check.

What happens if a collections agent breaks FDCPA?

An FDCPA violation can expose the collector to legal liability, penalties, and reputational damage, and a voice agent that systematically skips a disclosure or discloses to the wrong party multiplies that risk across every call. That is why compliance behaviors are tested as hard gates: the cost of shipping an untested agent is legal, not just a worse caller experience.

How do you test a voice agent with hostile callers?

Create caller profiles that are defensive, abusive, and manipulative, and drive them through the collection flow. Assert the agent stays professional, does not make threats or false statements, and still executes required disclosures and dispute handling under pressure. Composure is part of compliance in collections, so hostile-caller scenarios belong in the core suite, not as an afterthought.

What metrics matter for collections voice agents?

The dominant metrics are compliance ones, mostly binary: disclosure compliance, right-party contact accuracy, and dispute and cease-and-desist handling. Alongside them, track conduct under pressure and compliant resolution rate. Because a single systematic compliance miss is legal exposure, these metrics are release blockers rather than numbers to improve gradually over time.

How do you test cease and desist handling?

Insert a cease-and-desist or stop-contact request at different points in the call, including mid-negotiation, and assert the agent complies immediately and routes correctly rather than continuing to collect. Test both explicit phrasing and indirect requests. Honoring these is a legal obligation, so the test should treat any failure to stop as a release-blocking defect.

Related Articles

How to automate voice agent testing: synthetic callers vs manual QA

Learn how ai test automation replaces manual QA for voice agents. Compare synthetic callers vs human testers, with a 5-step framework to scale without hiring.

Read more

AI Agent Testing vs Voice Agent Testing: What General Tools Miss for Voice

AI agent testing measures text outputs. Voice agent testing measures behaviour through an acoustic pipeline. Five failure categories general tools miss.

Read more